Triple Net Listings Lie and Only True Cap Rate Matters

Triple net listings in commercial real estate routinely overstate what a landlord actually collects. For investors underwriting 1031 exchange replacement properties, the gap between a listed cap rate and the true net cap rate matters. That gap determines whether the deal actually works.

AC exclusions, HOA capital assessments, and vague purchase agreement language can quietly compress returns before you close. The marketing package will not tell you any of it.

Triple net listings frequently overstate what the landlord actually nets. AC exclusions, HOA capital assessments, and vague purchase agreement language can erode a cap rate before you close. The only number that protects your capital is the one you back into yourself from verified true net income.

What Triple Net Means in Practice

Triple net means the tenant pays property taxes, building insurance, and maintenance in addition to base rent. Absolute triple net pushes all expenses, including structural and capital items, to the tenant, with zero landlord exposure. That clean version also appears in listing language far more often than in actual leases.

NNN lease structures vary deal by deal. The gap between “listed as triple net” and “actually triple net” can be significant. HVAC systems are a common carve-out. Tenants pay a deductible. The landlord absorbs everything above that threshold. In desert markets where AC runs hard year-round, that single lease line can represent thousands in unmodeled annual expense.

When you back into value from a target cap rate, it must reflect actual cash flow, not marketing assumptions. For 1031 buyers, the tight timelines and requirements make accurate underwriting even less negotiable.

HOA Fees and Capital Assessments

Commercial condos carry a layer of complexity that catches out-of-market buyers off guard. When a property is within an HOA, you are not just underwriting the leases; you are also underwriting the HOA. That means transfer fees, capital improvement assessments, and community-level charges that activate at closing.

In master-planned commercial corridors across Arizona, an HOA capital contribution fee tied to purchase price can come due at closing. That can reduce your effective basis and compress your yield before day one. If the purchase and sale agreement doesn’t specify who pays these fees, and many don’t, you’re negotiating blind.

For local business owners evaluating whether to own rather than lease, this same HOA math applies. The distinction between gross operating costs on paper and actual owner-operator costs is worth understanding before you sign anything.

Reading a Listing Package Is Not Underwriting

The work that prevents these problems happens before you go under contract. A well-prepared listing agent provides a complete package: lease abstracts, expense histories, HOA financials, and full disclosure documentation. When that package is thorough, most issues surface before they become leverage problems during escrow.

When it is not thorough, you reverse-engineer a deal from fragments while the clock runs. For a 1031 buyer in a 45-day window with a hard deadline, that scramble is expensive in more ways than one.

Randy Shuffler has spent over two decades underwriting commercial transactions across Lake Havasu City, Kingman, and the broader Arizona corridor. His CCIM designation reflects advanced training in investment analysis, and that depth shows when a deal starts peeling back layers.

“It said it was triple net. An absolute triple net means the tenants pay for everything: taxes, insurance, everything. But then you find out in the leases they’re not paying for AC. They just have a deductible. So the true cap rate’s really not there. And then we’re finding out the fees. And those HOA and community fees aren’t exactly identified, and who pays for what. It kind of turns into a big mess.” – Randy Shuffler, Founder and Principal Broker, Lake Havasu City Commercial at Realty ONE Group Mountain Desert.

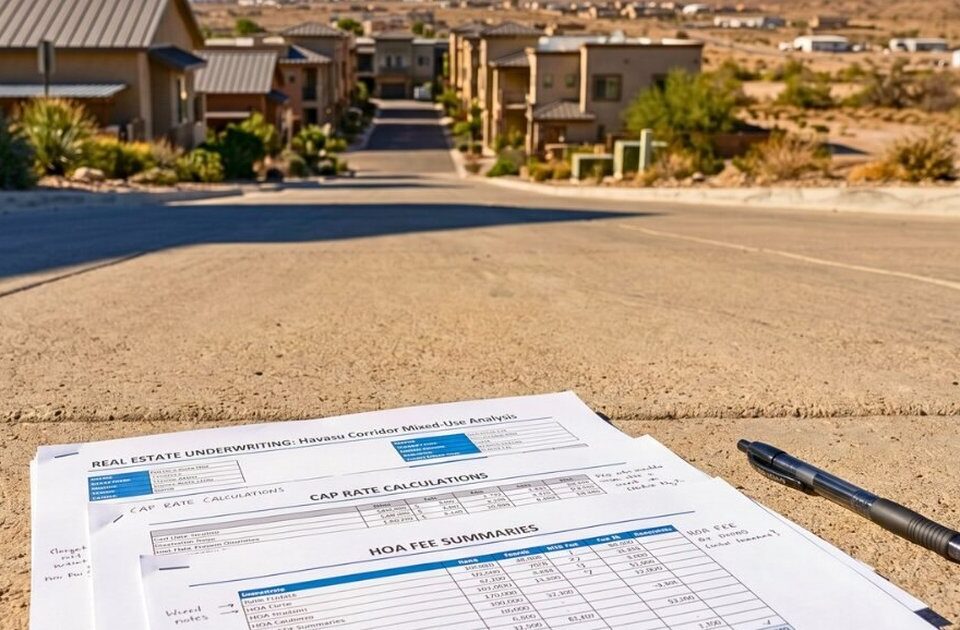

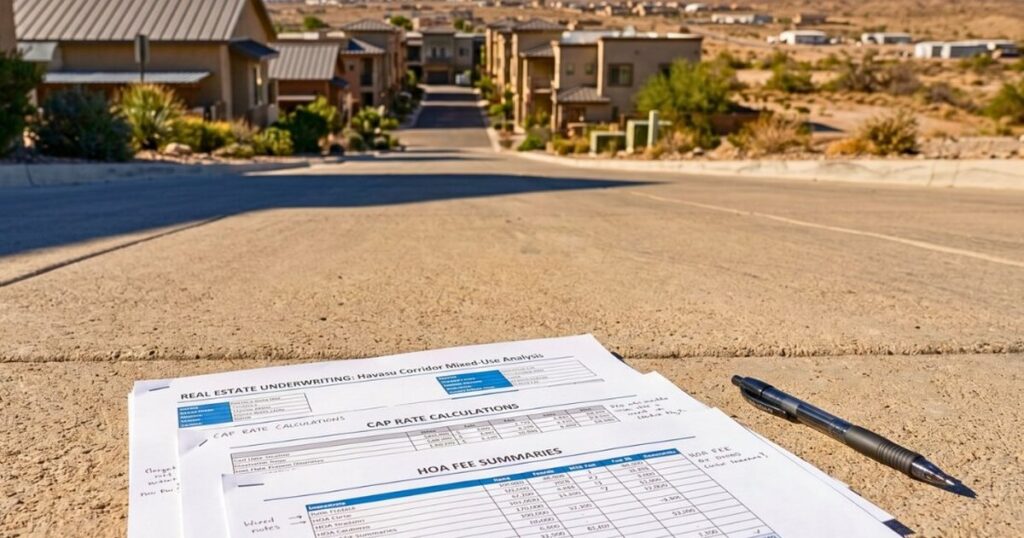

Backing Into True Net Cap Rate Value

Backing into value means starting from your target cap rate and calculating what you can pay based on verified net income. Do not accept the seller’s listed price and listed cap rate. You must derive the price the deal actually supports after accounting for every real expense, including:

- Lease carve-outs

- Management costs

- HOA fees

- Capital reserves

The difference between a 7.2% listed cap rate and a 6.1% true net cap rate on a $2 million property is roughly $180,000 in overpaid basis. That is not a rounding error. It is the spread between a sound investment and a corrective sale in three years.

The Appraisal Foundation’s Uniform Standards of Professional Appraisal Practice (USPAP) governs how income property values are formally derived. The methodology relies on verified income, verified expenses, and a defensible cap rate applied to the net result.

What to Do Before the 1031 Clock Starts

The most expensive mistake a 1031 buyer makes is starting the replacement search after the sale closes. By day one of the 45-day identification window, you should already know your target markets, underwriting criteria, and shortlisted properties worth pursuing.

That means running true-net analysis on candidates before pressure arrives. It means working with a local advisor who has already walked those corridors. They know which listings are clean and which require excavation. Ultimately, they can tell you on day one whether a deal carries a real cap rate or just a listed one.

“You really want to know your market and properties before you even sell your building in California. Once you’re selling it, you need to be putting out your feelers at that point. That way, when the 45-day identification process begins, you are not starting from zero. It’s stressful. Talk to a good agent who knows the market, put your feelers out everywhere.” – Randy Shuffler, Founder and Principal Broker, Lake Havasu City Commercial at Realty ONE Group Mountain Desert.

Buyers who pre-underwrite a shortlist enter the 45-day window with options and leverage rather than urgency. The ones who start from zero on day one often close on the wrong deal or miss the window entirely.

NNN Lease and 1031 Questions Answered

How do I calculate the true net cap rate on a triple-net property?

Start with gross scheduled income, then subtract all real operating expenses you will incur as the owner. Make sure to include items the lease assigns to the tenant that have dollar caps or carve-outs. Finally, factor in HOA fees, property management, and any capital reserves not covered by tenants. Divide the resulting net operating income by your purchase price. That is your true net cap rate, not the number in the brochure.

What HVAC lease language should I look for before buying an NNN property?

Look for how HVAC responsibility is defined in each lease. In many NNN structures, tenants pay only a repair deductible, leaving the landlord to absorb costs above that cap. Get the actual dollar threshold, the age and condition of each system, and an estimate of remaining useful life. In Arizona’s desert climate, commercial HVAC systems work harder and fail faster than in moderate climates.

What should a complete due diligence package include for a commercial NNN deal?

A complete package includes lease abstracts with amendments and two years of actual expense history. If applicable, include HOA financials and meeting minutes. Finally, secure current insurance declarations, tax bills for the past two years, and any existing disclosures or inspection reports. If the listing agent cannot provide this before you go under contract, that gap is its own data point.

How does the lease structure affect resale value in a triple net property?

Lease structure determines what a future buyer will underwrite. Weak lease terms, such as carve-outs, caps, short terms, or personal guarantees, compress resale cap rates and reduce exit prices. The lease is the income stream. How well it is documented and how clearly expenses are assigned determines how confidently the next buyer can underwrite it.

Can HOA fees be negotiated in a commercial purchase agreement?

Yes. Who pays HOA transfer fees, capital contributions, and outstanding assessments is negotiated in the purchase and sale agreement. The problem is that many buyers do not identify these fees until escrow, when they have less leverage. The fix is to request the full HOA financial package, including pending assessments and approved capital projects, before making an offer.

What is a realistic cap rate range for Arizona Triple Net commercial properties right now?

In stabilized Arizona markets, well-documented NNN properties with credit tenants and long lease terms trade at low-to-mid 6% cap rates. Properties with shorter terms, local tenants, or landlord-exposed lease terms trade at higher cap rates to reflect added risk. A listed 7.5% cap rate with a messy lease structure often underwrites to 6.2% or lower once real expenses are modeled.

How do I verify that a replacement property’s in-place rents are at market?

Request a current rent roll, then cross-reference each unit against comparable lease comps in the same submarket. If in-place rents are significantly above market, model what happens when those leases roll. Above-market rent resetting at renewal can compress income and force a repricing at the wrong time. You can learn more in a piece I wrote about how strong in-place rents can be a red flag.

Get the Numbers That Matter

Triple-net labels create confidence that the lease structure often does not support. HVAC exclusions and vague expense language can shift costs back to the landlord. The difference between what’s listed and true net income determines whether the deal works.

Shuffler Commercial Realty works with investors to analyze lease structures line by line to uncover hidden exposure. Our goal is to help investors base decisions on real numbers. Reach out to my team to run a true-net analysis before you commit.

Randy Shuffler is the founder of Lake Havasu City Commercial at Realty ONE Group Mountain Desert. He holds the CCIM designation, earned by fewer than 6% of commercial real estate practitioners. He has spent over 20 years underwriting commercial transactions across Lake Havasu City, Kingman, and Mohave County. His background includes a BS in Finance from San Diego State University.

ABOUT THE EXPERT

Randy Shuffler | Founder & Principal Broker, Lake Havasu City Commercial | CCIM | 20+ years in real estate & finance | $5M+ in verified sales | 52,000+ sq ft transacted | BS Finance, San Diego State University | Realty ONE Group Mountain Desert

{kind=link}

{kind=link}

{kind=link}